Building a Powerful and Coherent Vision for Net Zero in Asia

Discussion Paper

October 14th, 2022

Our planet’s future is at a critical juncture. The world must peak global emissions by 2025 and reduce them to net zero by the middle of the century to maintain a reasonable chance of achieving the Paris Agreement’s 1.5°C target, according to the latest science from the UN's Intergovernmental Panel on Climate Change (IPCC). This will require major transitions across all sectors of the economy to slash fossil fuel use, promote widespread electrification, switch to cleaner fuels, and improve overall efficiency.

What happens in Asia will be crucial. The region is home to more than half of the world’s population as well as more than half of emissions. Asia’s high economic growth and comparatively low per capita emissions mean that immediate and ambitious action to decouple economic growth from emissions is needed for the world to achieve the Paris Agreement’s temperature goals. The consequences otherwise would be devastating — especially for Asia, which is already disproportionately exposed to climate impacts like floods, droughts, and heat waves.

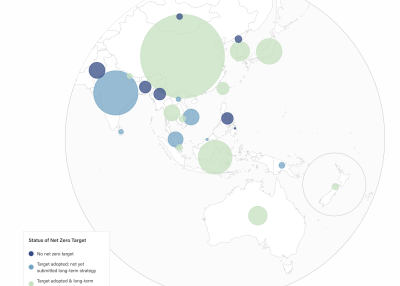

Asian countries are already stepping up with ambitious climate pledges and net zero targets. Among the region’s major emitters, a number of countries including Japan, South Korea, and Australia are already aiming to reach emissions neutrality by mid-century in line with a 1.5°C pathway. Others have adopted net zero targets though with timelines that lag behind this level of ambition — notably China, Indonesia, and India. Implementation will also require improved governance: only nine countries out of more than 50 in the UN’s Asia-Pacific Group have net zero targets that are legislated or included in official policy documents.

The High-level Policy Commission on Getting Asia to Net Zero launched earlier this year to help build a powerful, coherent, and Paris-aligned regional vision for net zero emissions in the Asian region. Through research, analysis, and engagement, the Commission’s diverse set of recognized Asian leaders aims to urgently accelerate Asia’s transition to net zero emissions while ensuring that climate action boosts the region’s economy, trade, interconnectedness, and livelihoods. The Asia Society Policy Institute serves as the Commission’s secretariat.

To shed light on how Asia can fully tap into the benefits and opportunities of ambitious climate action, the Commission has partnered with Cambridge Econometrics to model the macroeconomic implications of existing climate pathways as well as scenarios with greater ambition. This research also pinpoints the challenges and costs of implementation to help policymakers and other stakeholders adopt constructive solutions and ensure a just transition for the region.

This initial document summarizes the first economic analysis to distill how, if fully implemented, the Asia-Pacific’s recent increase in climate ambition in the lead-up to and at COP26 will impact the region as compared to a baseline scenario of preexisting policies. This issue paper focuses on the Asia-Pacific economy as a whole, providing a pan-regional context to complement forthcoming studies on India and Indonesia, as well as more ambitious pathways for the Asia-Pacific region. Future research intends to expand the geographic scope to include other areas of Asia, as well as other aspects of the transition, such as specific sectors and issues.

Seizing the benefits of Asia’s climate transition

Asia’s emissions are largely driven by power generation systems that are heavily dependent upon fossil fuels, especially coal. While the share of fossil fuels in global power generation is 63 percent, a number of major Asian economies, such as China and India, have a notably higher share. Slow electrification of transport and a high share of energy-intensive industries in economic output also contribute to high emissions. However, the faster than expected uptake of renewables, especially solar PV in the power sector, has slowed down the pace of emissions growth in recent years.

In the baseline scenario where Asia-Pacific governments do not adopt new climate policies, the Asia-Pacific region is projected to experience strong GDP growth of above 4.2% per annum (pa) over 2020-2040. Most countries have growing or constant emissions in the modeled period. The power sector drives the pattern of overall emissions where fossil fuels continue to make up a high share of the capacity mix, especially in China and India.

The good news is that the Asia-Pacific’s most recent climate commitments, if realized, would considerably boost the region’s economic growth, employment, and trade balance as compared to a baseline scenario. When additional policies are adopted to fully implement the most recent Nationally Determined Contributions (NDCs) and net zero targets, the Asia-Pacific region benefits significantly as follows:

Enhanced economic growth: Achieving COP26 commitments can lead to 5.4% greater GDP by 2030 than the trajectory implied by currently enacted pre-COP26 policies. Impacts are smaller in the long run but still equate to 2.0% of additional output in 2060. The GDP impacts are driven mainly by higher levels of investment in the power sector, energy efficiency, and carbon sinks.

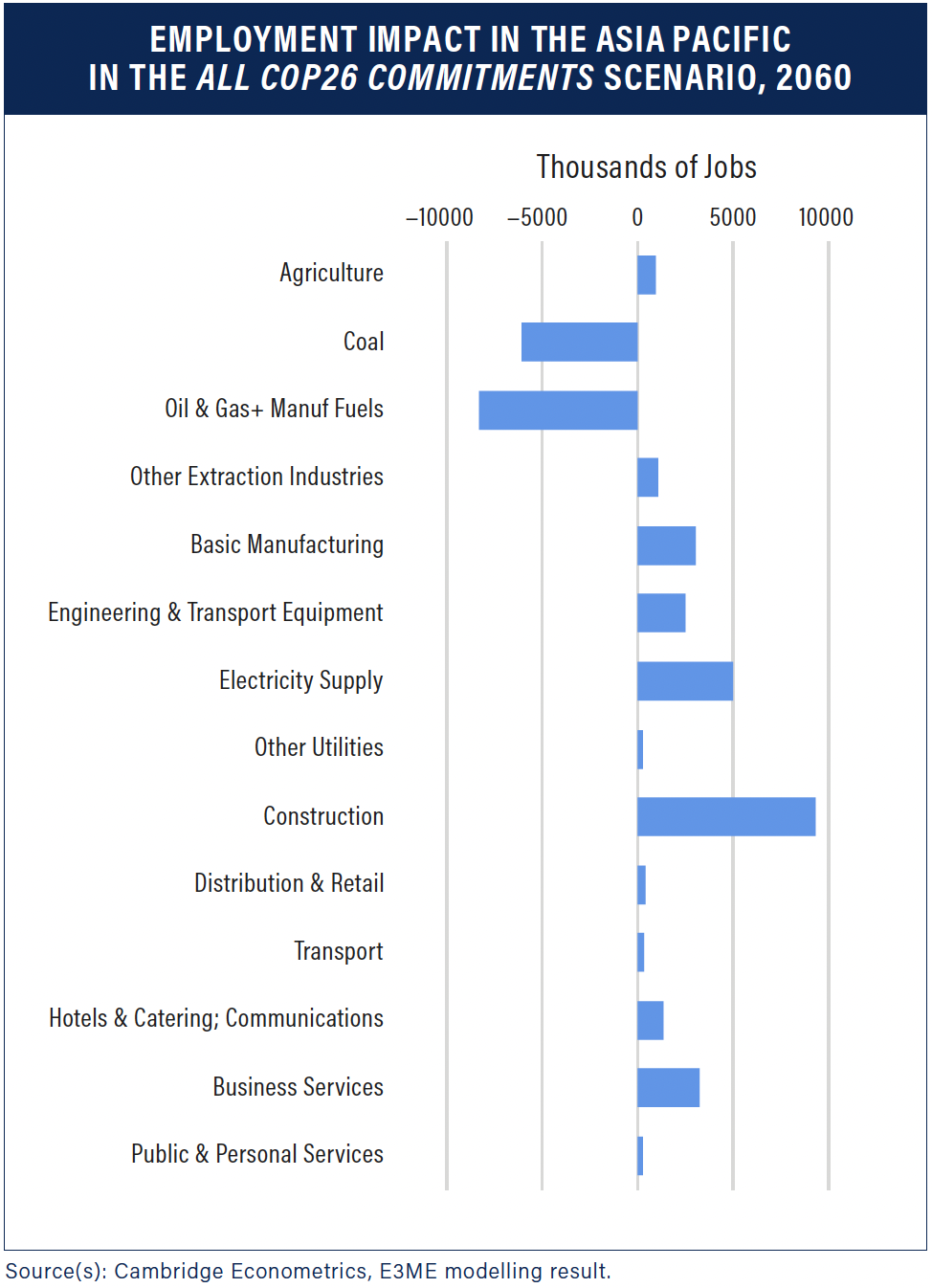

Increased employment: Employment is estimated to be 1.5% higher than baseline in 2031 (when the impact peaks), and 0.7% higher than baseline in 2060. This is equivalent to 34 million additional jobs in the Asia-Pacific in 2060, despite notable job losses in the fossil fuel sector. There are substantial gains in sectors that form the supply chains of the technology transition, including construction, other extraction industries, and manufacturing sectors, as well as electricity supply. A higher level of aggregate employment in the COP26 commitments scenario relative to baseline also results in a higher level of income from employment for households.

Improved trade balance and energy security: Reducing the dependence on, and therefore the import of, fossil fuels also improves the Asia-Pacific’s trade balance by $533bn by 2060, which equates to slightly less than one-third of the long-term growth. This gain comes mostly from a reduction in fossil fuel imports. Imports of manufactured fuels, oil, and gas and coal are 71%, 58%, and 27% below the baseline levels, respectively, in 2060.

Reduced energy costs: Electrification of transport, energy efficiency, and falling energy intensity of production bring productivity improvements and savings for household energy costs. Implementing COP26 commitments would lead to savings of nearly 40% on household energy costs by 2050 and just under 30% by 2060 due to rebound effects and continued economic growth, equivalent to an absolute reduction of around $200bn across the Asia-Pacific region.

Constructively addressing Asia’s transitional challenges

However, the transition will come with trade-offs. The research identified several key challenges that accompany the aforementioned benefits. The following areas will all require coordinated and constructive attention from policymakers to safeguard livelihoods and ensure as smooth a transition as possible:

Significant required investment: Cumulative investment requirements for meeting announced net zero targets are estimated at $53.5trn from now until 2060, with much of this investment concentrated in China and India as the largest emerging economies. The peak of low carbon investment across the region is expected in the early 2030s when investment is 14.1% higher than in the baseline scenario. International financial support for developing countries would free up domestic finance for development, poverty reduction, and management of social impacts.

Fossil fuel job losses: Despite net gains in employment, significant job losses occur in fossil fuel supply sectors (coal and oil and gas) due to the transition to renewables. Social policies, such as reskilling schemes to allow workers to take advantage of employment opportunities created in the transition, will be needed in order to deliver a just transition in the Asia-Pacific.

Impacts on households: When the transition is financed by domestic government revenues or private investments, the impacts of both lower purchasing power and higher tax burden outweigh the positive impact on nominal income for households. As a result, there is a net negative impact on household income and consumption, implying that consumers directly bear some of the cost burden of the transition.

Moreover, the Asia-Pacific’s near- and mid-term climate commitments are not yet ambitious enough to align with the Paris Agreement’s goals with limited or no overshoot. According to the modeling, the region will reduce its carbon emissions by only 21% below 2010 levels by 2030 based on all commitments made through COP26. This figure lags behind the IPCC’s findings that global net anthropogenic CO2 emissions decline by about 45% from 2010 levels by 2030 for no or limited overshoot of 1.5°C, with about 25% reductions by 2030 for a below 2°C world.

Asia’s moment to lead the way to a more prosperous future

Asia is fortuitously entering a stretch in the global limelight during which it will host a series of global platforms from which it can lead the climate transition by example and bring other countries along. During 2022 and 2023, Asia will host G20 meetings in Indonesia and India, the G7 summit in Japan, and the UN’s COP28 climate summit in the United Arab Emirates.

To lead the global transformation to a clean economy — and to take full advantage of the benefits of accelerated climate ambition like enhanced economic growth, increased employment, and improved energy security — Asian countries must cooperate on three core steps.

First, alignment. Asian nations must come together to form a united voice around their common interests. This has been done before — for instance, in 1994 when Asia-Pacific Economic Cooperation leaders committed to reduce trade and investment barriers and promote the free flow of goods, services, and capital. A joint commitment to climate action can similarly boost the region’s economic and social prosperity. If delivered now while Asia is in the global limelight, it can also set the tone for other regions to follow suit.

Second, ambition. Most large Asian economies have committed to reaching net zero emissions, but with varying timelines and levels of supporting detail. The Glasgow Climate Pact calls on countries to revisit and strengthen their targets before COP27 in November 2022 to keep the world on track to limit global warming to 1.5°C. By doing so, Asia can attract more investment, maximize benefits such as jobs and energy security, and limit climate impacts.

Third, implementation. Asian countries must demonstrate political will by reforming policies and developing roadmaps to achieve their climate goals. This will de-risk investments and attract finance, technical support, and other resources through initiatives like the Just Energy Transition Partnerships proposed by the G7.

If implemented in full, the Asia-Pacific’s climate commitments could bring the region to net zero emissions by 2056, according to the modeling. While this will require significant investment, the dividends are clear. Asian leaders understand the urgency we face better than many, because their region is already living in the era of climate crisis.

This year, millions of people in India, Bangladesh, and Pakistan have felt extreme heat, which forced a ban on wheat exports in India and caused power outages. Massive floods in southern China wiped out homes, ruined crops, and shut down manufacturing factories, while extreme heat in the north and center caused cement roads to rupture. Ensuring that mitigation and adaptation investments go hand-in-hand can help limit and build resilience to these and other climate change impacts.

We saw countries come together to build the Paris Agreement over several years. Asia must now stand ready to help turn Paris’s landmark goals into reality and keep global temperature increases this century within 1.5°C.